What the Tax Cuts and Jobs Act Means for 1099 Clinicians

Recently, I overheard a conversation between several CRNAs discussing tax strategies shared by a CPA. One clinician mentioned she was told she could “get creative” and expense leisurely trips, dinners, and entertainment such as concerts.

I understand the appeal. As a 1099 clinician, legitimate business deductions can meaningfully reduce your tax bill.

But one comment stood out: deducting entertainment expenses.

Since 2018, the Tax Cuts and Jobs Act (TCJA) has generally eliminated the deduction for entertainment expenses—and that remains true today.

Let’s review what changed, what the rules are now, and what locum tenens CRNAs and physicians should watch for.

What Changed Under the Tax Cuts and Jobs Act?

Pre-2018: Entertainment Was Partially Deductible

Before 2018, businesses could generally deduct 50% of entertainment expenses if they were directly related to the active conduct of a trade or business or associated with a substantial business discussion (IRS Publication 463, prior editions).

For example, if sporting event tickets cost $200, $100 might have been deductible under prior law.

Post-2018: Entertainment Is Generally Not Deductible

Beginning in 2018, the TCJA permanently eliminated the deduction for expenses related to entertainment, amusement, or recreation (Internal Revenue Code §274 as amended by TCJA).

That includes:

Even if business is discussed, the entertainment portion is generally nondeductible (IRS Publication 463, current edition; final regulations under T.D. 9925).

In plain terms: discussing a locums contract during a Knicks game does not make the ticket deductible.

Business Meals vs. Entertainment: Critical Distinction for 1099 Clinicians

This is where confusion often arises.

While the TCJA eliminated entertainment deductions, it did not eliminate the deduction for business meals.

According to IRS guidance, taxpayers may generally deduct 50% of the cost of business meals if:

(IRS Publication 463, current edition; final regulations incorporating Notice 2018-76)

If food and beverages are purchased at an entertainment event, they may still be deductible—but only if they are purchased separately or separately stated from the entertainment cost.

The key takeaway: meals and entertainment are treated differently under current law. (Note: A temporary 100% deduction for certain restaurant-provided meals expired after 2022; the standard 50% limit now applies to most business meals, including travel and client meals for independent contractors.)

Tax Deductions for Locum Tenens CRNAs and Physicians

As a 1099 CRNA or anesthesiologist, you are effectively running a small business.

That means:

The locums model also creates legitimate deductible expenses, such as:

However, the line between business and personal expenses can blur—especially when:

Being away from home for work does not automatically convert every expense into a deductible business cost. Proper substantiation (e.g., records showing business purpose, receipts, logs of dates/locations/attendees/purpose) is essential to defend these deductions in an audit.

The “Ordinary and Necessary” Standard

The IRS requires that business expenses be both ordinary and necessary (Internal Revenue Code §162).

That standard does not mean “creative.” It means defensible.

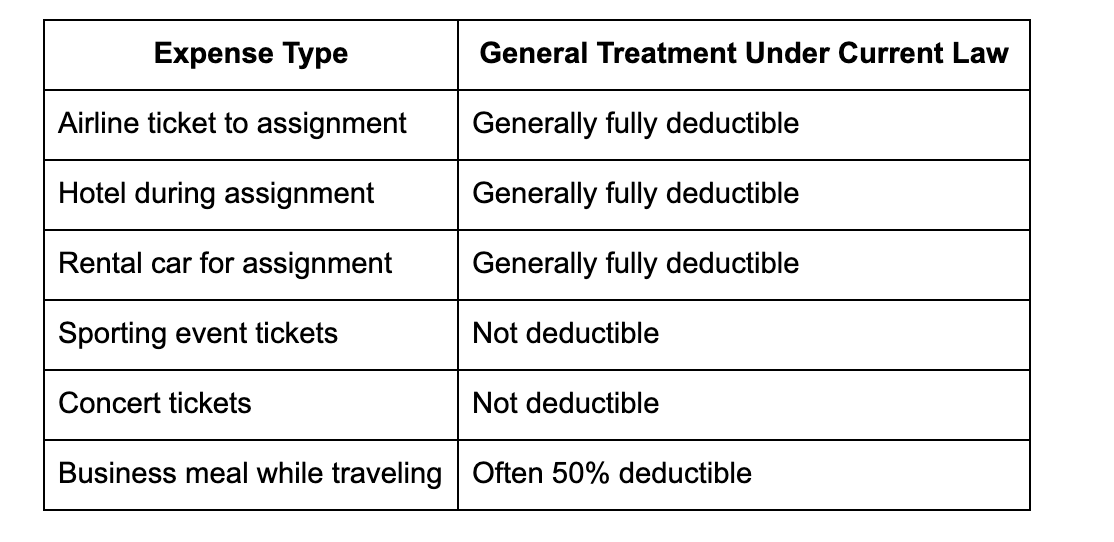

High-Level Examples Under Current Law

Expense Type

These descriptions are general in nature and depend on individual facts and circumstances.

Why “Write Off Everything” Is Risky Advice

Entertainment deductions have generally been disallowed since 2018. Attempting to recharacterize concerts or sporting events as deductible business expenses is difficult to support under current law.

More importantly, meaningful tax strategy for high-income clinicians rarely hinges on entertainment tickets.

For 1099 CRNAs and physicians, larger planning opportunities often include:

In that context, a $500 concert ticket is usually insignificant. Misclassification, however, can create unnecessary exposure.

Final Thoughts: Running Your Locums Career Like a Business

Operating as a locum tenens clinician means operating a business.

That includes:

Tax rules evolve—just as we’ve seen in other complex areas like student loan repayment programs. Staying current matters.